SaaS Market Trends 2026: 50+ Stats and Data Points

SaaS market trends 2026 in 50+ stats: market size, AI-native growth, vertical SaaS, pricing shifts, and adoption data for founders and buyers.

The global SaaS market sits somewhere between $375 billion and $465 billion in 2026, depending on who you ask. Fortune Business Insights puts it at $375.57 billion. Precedence Research pegs it closer to $465 billion. The gap is wide because each firm counts "SaaS" differently. But every major analyst agrees on the direction: up, and fast, with the market on track to clear $1 trillion before 2035.

This is a stats roundup, not a think piece. Below you will find 50+ data points on SaaS market trends 2026, grouped by theme. Market size. AI adoption. Vertical and micro-SaaS. Spend and waste. Pricing. Regional shifts. Marketing. Each number is attributed to its source so you can cite it or check it.

If you build, buy, or invest in software, these are the figures shaping your year.

Fast facts about Saas market

The SaaS market reached roughly $315.68 billion to $408 billion in 2025, according to estimates.

99% of organizations now run at least one SaaS application.

More than 30,800 SaaS companies operate worldwide; about 17,000 sit in the United States.

75% of SaaS companies have already shipped AI features.

The AI-created SaaS market could hit $770 billion by 2031 at a 40.2% CAGR.

Vertical SaaS grows at 18% to 32% a year versus 12% to 15% for horizontal tools.

About 51% of purchased SaaS licenses go unused.

85% of SaaS companies now use some form of usage-based pricing.

SaaS market size and growth in 2026

The headline number depends on the source. Different firms use different scopes, so the spread is real and worth showing.

Why the gap? Some firms count only public-cloud SaaS. Others fold in AI-native platforms and B2B-only segments. Reading the definition before you trust the number makes more differentiations.

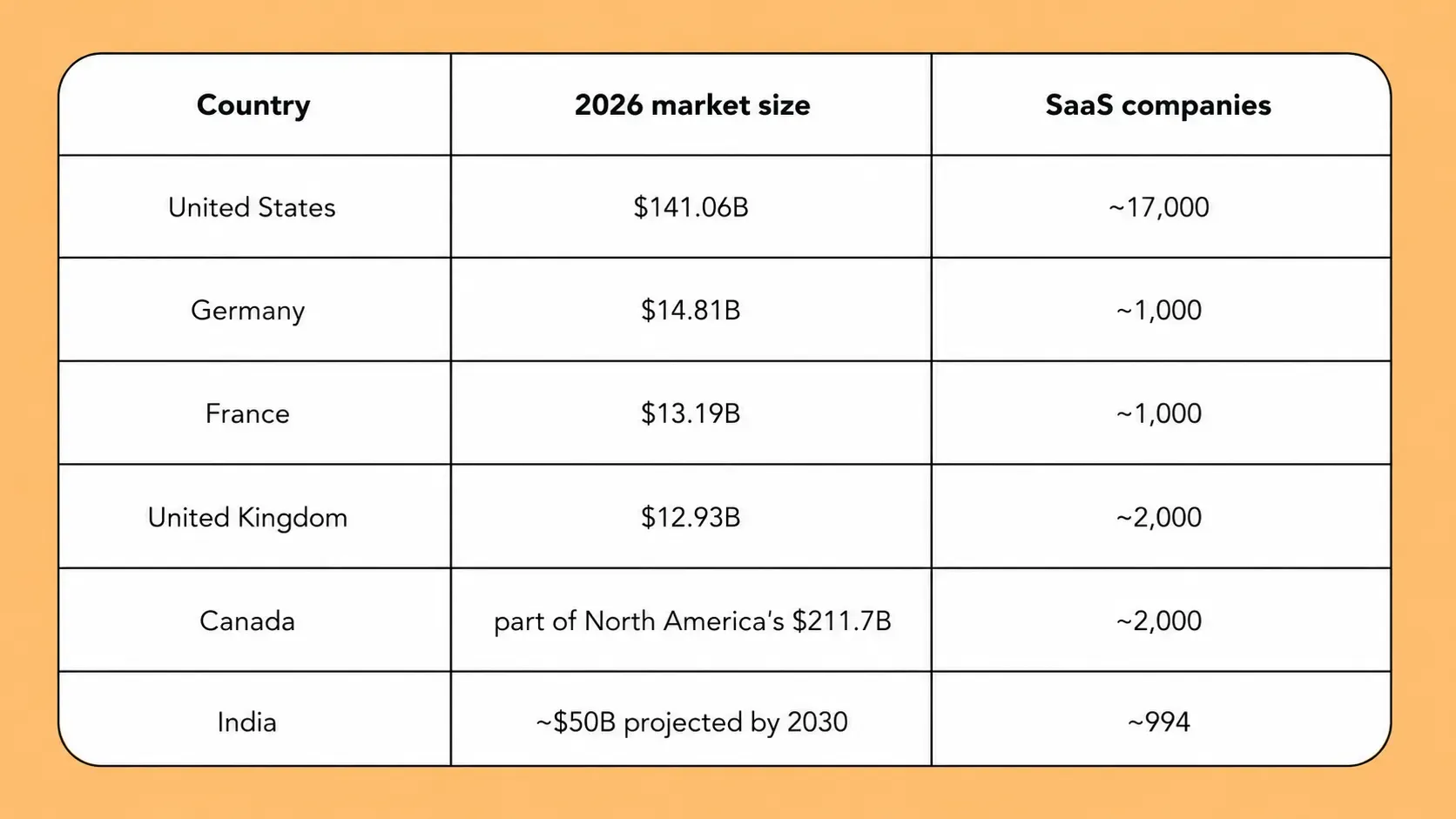

A few points hold steady across sources. North America led with a 46.9% share of global SaaS revenue in 2025. The U.S. market alone is set to reach $141.06 billion in 2026. Gartner ranks software as the fastest-growing IT spend category for 2026, up 14.7% year over year.

Public cloud spend gives more context. End-user spending on public cloud services hit $723.4 billion in 2025, up from $595.7 billion the year before, and SaaS is the largest slice of that pie.

AI reshapes SaaS products and pricing

AI is no longer a feature. It is the main growth story, and it splits the market into two.

Adoption is near-total. By 2026, more than 80% of companies are expected to run AI-enabled apps, up from just 5% in 2023. Around 75% of SaaS firms have already shipped AI features, and 92% plan to add more.

The money follows the trend:

The AI-created SaaS market could reach $770.32 billion by 2031, growing 40.2% a year.

AI-powered SaaS grows roughly 3x faster than traditional SaaS.

AI-native companies raise at 40% higher valuations than legacy SaaS, with median Series B rounds near $175 million in late 2025.

Top AI-native firms hit about $40 million in ARR within year one and pass $120 million by year two.

There is a darker line in the data, too. Forward price-to-earnings multiples for public SaaS fell from 84.1x at the 2020 to 2022 peak to 22.7x by March 2026. For the first time, that sits below the broad S&P 500. Investors are nervous that per-seat licensing cannot survive an agentic AI world.

The next shift is agents over copilots. IDC expects agentic AI to absorb more than 26% of worldwide IT spend over five years, reaching $1.3 trillion by 2029. By late 2025, 33% of large organizations had already deployed agentic AI.

Vertical and micro-SaaS lead growth

Generic, one-size-fits-all software is losing steam. Industry-specific tools are winning.

Vertical SaaS grows at 18% to 32% a year, against 12% to 15% for horizontal platforms (Modall, citing SaaStr). It now makes up about 35% of total SaaS revenue. Mordor Intelligence sizes the vertical market at roughly $164 billion in 2026.

Why verticals win comes down to economics. They command 2x to 3x higher contract values than horizontal tools because the fit is tighter. Embedded finance lets them capture transaction revenue on top of subscriptions, lifting revenue per customer by 2x to 5x. And AI trained on industry data builds a moat that broad tools cannot copy.

Healthcare, construction, legal, agriculture, and financial services drive the fastest gains. These are analog-heavy fields with a long runway to digitize.

Micro-SaaS is the lean cousin of this trend. These are small, single-problem tools, often run by solo founders:

Micro-SaaS products grow at around 25% a year, faster than traditional SaaS.

Profit margins can reach 80% thanks to low overhead.

Founders using organic channels keep customer acquisition cost near $0 to $50, versus $200 to $600 for paid.

Divtechnosoft has built in this exact lane, from a multi-tenant real estate CRM SaaS to gym management platforms. You can see the full set in our case studies.

SaaS spend, adoption, and waste

Adoption is saturated. The story now is sprawl and cost control.

Nearly every company uses SaaS. 99% of organizations run at least one SaaS app. About 81% have automated at least one business process with it.

But the app count is large and often unmanaged:

The average company runs 106 to 291 SaaS apps, depending on the dataset.

Large enterprises with 10,000+ staff average 473 apps.

SaaS spend per employee rose to about $5,607 a year, up 7% from 2023.

Waste is the hidden tax. An estimated 51% of purchased licenses go unused, the highest rate on record. BetterCloud and others put annual SaaS waste near $18 billion.

So budgets are tightening. 42% of organizations cut SaaS budgets due to economic pressure, pushing teams to optimize what they own instead of buying more. Consolidation is real, but slowing. The average app count dropped from 112 in 2023 to 106 in 2024, yet the consolidation rate fell from 14% to just 5%.

Pricing shifts from seats to usage

The per-seat model is fading. Pricing now tracks value delivered, not headcount.

About 85% of SaaS companies use some form of usage-based pricing in 2026. Outcome-based pricing, where fees tie to results like tickets resolved, is climbing toward 40% adoption from around 15%.

Retention now matters more than raw growth. Net Revenue Retention has become the primary health metric, with best-in-class firms above 120%. Yet only 16% of private SaaS companies consistently clear the Rule of 40. That benchmark, where growth plus profit margin tops 40%, is now a key signal for investors.

Security expectations rose with the stakes. The average data breach costs $4.44 million, and SOC 2 Type II is now a baseline, not a selling point.

SaaS market by region and country

The United States leads by a wide margin, but the growth curve is steepest in Asia-Pacific and Latin America.

By region, North America held 46.9% of global SaaS revenue in 2025. Europe holds roughly 25% to 28%. Asia-Pacific accounts for about 18% but grows fastest, with revenue projected to rise at a 20.94% CAGR through 2029 to reach $104.25 billion. Latin America is set to double from $21.4 billion in 2024 to $45.1 billion by 2030.

The country-level picture shows where the money and the vendors sit:

A few country notes add context. The U.S. holds roughly 55% of all SaaS companies worldwide and serves a global customer base, not just a domestic one. Across Europe, 63% of SMEs now use at least one cloud-based application. India posts one of the highest growth rates, with its SaaS sector tracking toward $50 billion by 2030 and private equity inflows of $1.38 billion in just the first seven months of 2025. China's market is set to grow from $14.53 billion in 2024 to $37 billion by 2029, while the GCC market in the Middle East stood at $7.14 billion in 2025.

For vendors selling across borders, the lesson is plain. The U.S. remains the largest and most mature buyer base, Europe rewards privacy-ready products, and APAC and Latin America offer the fastest new demand.

SaaS marketing moves to AI search

How buyers find software changed faster than most teams adjusted. This shift defines SaaS marketing trends for 2026.

Buyers ask AI first. 71% of B2B SaaS buyers now lean on AI chatbots to research software. 89% of B2B buyers use generative AI during purchasing research. AI Overviews show up on 48% of Google queries as of April 2026.

That rewires what wins traffic:

AI search visitors convert at 4x to 5x the rate of traditional organic traffic.

Content with statistics earns 28% to 40% higher visibility in AI search.

44.2% of AI citations come from the first 30% of a page's text.

B2B SaaS sites with original research pull 29.7% more organic traffic than those without, at 9.3%.

Costs keep climbing. Customer acquisition cost has jumped 60% to over 200% in competitive markets in recent years. The counter is content that compounds. B2B SaaS SEO averages a 702% ROI with a 7-month break-even over a three-year window.

The takeaway is simple. Publish original data. Structure pages as clear answers. Get cited by the AI that buyers now trust.

What the numbers mean for SaaS builders

Strip away the noise and three signals stand out for 2026.

First, specificity beats breadth. Vertical and AI-native products grow faster, retain better, and price higher. If you are scoping a new product, a sharp niche is the safer bet than another horizontal tool.

Second, AI is now table stakes, but adoption alone is not a moat. Proprietary data and real workflow ownership are. Bolting a chatbot onto a generic app will not move the needle.

Third, efficient growth wins funding and trust. NRR, the Rule of 40, and usage-based pricing reward teams that ship value, not just features.

This is the work we do at Divtechnosoft. We help founders and SMBs turn market insight into shipped products, often as an MVP in six to eight weeks, with AI built in from day one. Explore our SaaS and AI development services if you are ready to build for where the market is heading, not where it has been.

Frequently asked questions

How big is the SaaS market in 2026?

Estimates range from $375.57 billionto $465.03 billion. The gap reflects different definitions of what counts as SaaS. Most forecasts have the market passing $1 trillion before 2035.

What is the fastest-growing SaaS segment?

AI-native and vertical SaaS. AI-created SaaS is projected to grow above 40% a year, while vertical SaaS grows 18% to 32% a year versus 12% to 15% for horizontal tools.

How much of SaaS is AI-powered now?

About 75% of SaaS companies have shipped AI features, and more than 80% of companies are expected to run AI-enabled apps in 2026, up from 5% in 2023.

Is vertical SaaS better than horizontal?

For growth and retention, the data favors vertical. It commands 2x to 3x higher contract values and builds deeper moats. Horizontal tools still serve broad needs but face saturated, crowded markets.

Why do SaaS market size estimates differ so much?

Each research firm sets its own scope. Some count only public-cloud SaaS. Others include AI-native platforms, B2B-only segments, or adjacent cloud services. Always check the definition behind a figure before you cite it.